Fill Out a Valid IRS 1099-MISC Template

Guide to Writing IRS 1099-MISC

After gathering all necessary information, you can begin filling out the IRS 1099-MISC form. This form is used to report various types of income received by individuals or businesses that are not classified as wages. Make sure you have accurate details before proceeding to ensure compliance with tax reporting requirements.

- Obtain a blank IRS 1099-MISC form. You can download it from the IRS website or order physical copies.

- In the top left box, enter your name, address, and taxpayer identification number (TIN). This is typically your Social Security number or Employer Identification Number.

- In the top right box, enter the recipient's name, address, and TIN. Verify this information for accuracy.

- In Box 1, report any rents paid to the recipient. Include the total amount paid during the tax year.

- In Box 2, enter any royalties paid. Ensure the amount is correct and reflects the total for the year.

- For Box 3, report other income. This can include various payments not covered in other boxes.

- In Box 4, withholdings should be reported if applicable. This may include federal income tax withheld.

- Complete Boxes 5 through 7 if relevant. These boxes cover fishing boat proceeds, medical and healthcare payments, and nonemployee compensation, respectively.

- At the bottom of the form, check the appropriate box to indicate if you are reporting payments made in the prior year.

- Sign and date the form. Ensure that you have completed all necessary sections before submitting.

- Send the completed form to the IRS by the deadline, which is typically January 31 for the previous tax year. Also, provide a copy to the recipient.

Document Breakdown

| Fact Name | Details |

|---|---|

| Purpose | The IRS 1099-MISC form is used to report various types of income other than wages, salaries, and tips. |

| Who Receives It | Independent contractors, freelancers, and other non-employees who receive payments of $600 or more in a year typically receive this form. |

| Filing Deadline | Taxpayers must file the 1099-MISC form with the IRS by January 31 of the year following the tax year. |

| State-Specific Forms | Many states have their own versions of the 1099-MISC form. For example, California requires the 1099-MISC to be filed under California Revenue and Taxation Code Section 18621. |

| Penalties for Non-Compliance | Failing to file or providing incorrect information can result in penalties. The IRS may impose fines based on the severity of the error. |

FAQ

What is the IRS 1099-MISC form?

The IRS 1099-MISC form is used to report various types of income received by individuals who are not classified as employees. This form is typically used by businesses to report payments made to independent contractors, freelancers, and other non-employees for services rendered. If you received $600 or more in a tax year for services, you should expect to receive a 1099-MISC from the payer.

Who needs to file a 1099-MISC form?

Generally, if you are a business or individual that has paid someone $600 or more for services, you are required to file a 1099-MISC form. This includes payments made to:

- Independent contractors

- Freelancers

- Consultants

- Rent payments

- Prizes and awards

However, there are exceptions. For example, payments made to corporations typically do not require a 1099-MISC unless they are for medical or legal services.

When is the deadline for filing the 1099-MISC?

The deadline for filing the 1099-MISC form varies depending on how you file. If you are submitting the form electronically, the deadline is March 31. For paper filings, the deadline is January 31. Make sure to send copies to both the IRS and the recipient by these dates to avoid penalties.

What information is required on the 1099-MISC form?

When completing the 1099-MISC form, you will need to include the following information:

- The payer's name, address, and Tax Identification Number (TIN)

- The recipient's name, address, and TIN

- The amount paid in the appropriate box (e.g., Box 1 for nonemployee compensation)

- Any applicable federal income tax withheld

Accurate information is crucial to ensure compliance and avoid issues with the IRS.

What should I do if I don’t receive a 1099-MISC form?

If you believe you should have received a 1099-MISC but haven't, reach out to the payer. It’s important to communicate with them to confirm whether they are required to issue one. If they confirm that they will not issue a 1099-MISC, you are still responsible for reporting the income on your tax return. Keep records of your income for accurate reporting.

What happens if I file the 1099-MISC form late?

Filing the 1099-MISC form late can result in penalties from the IRS. The amount of the penalty depends on how late you file:

- $50 if filed within 30 days of the due date

- $100 if filed more than 30 days late but by August 1

- $260 if filed after August 1 or not filed at all

Timely filing is essential to avoid these penalties and maintain good standing with the IRS.

Can I e-file the 1099-MISC form?

Yes, you can e-file the 1099-MISC form. In fact, e-filing is often recommended because it is faster and reduces the chance of errors. The IRS provides an online filing system, and many tax software programs also support e-filing for 1099 forms. Ensure that you have all the required information ready before you start the process to make it as smooth as possible.

Fill out Other Forms

Printable Medication Error Form Template - Patient-centered care is the priority in all medication error incidents.

Free Printable Time Sheets - Helps identify trends in employee attendance and punctuality.

Properly managing staff schedules is crucial for any organization, which is why utilizing the Employee Availability form can greatly enhance the scheduling process. By understanding when employees are available, employers can allocate shifts more effectively. To get started, you can access the Employee Availability Form and ensure that all preferences are taken into consideration.

Statement of Facts Ca Dmv - The DMV Reg 256 serves to clarify and certify the nature of vehicle transactions in California.

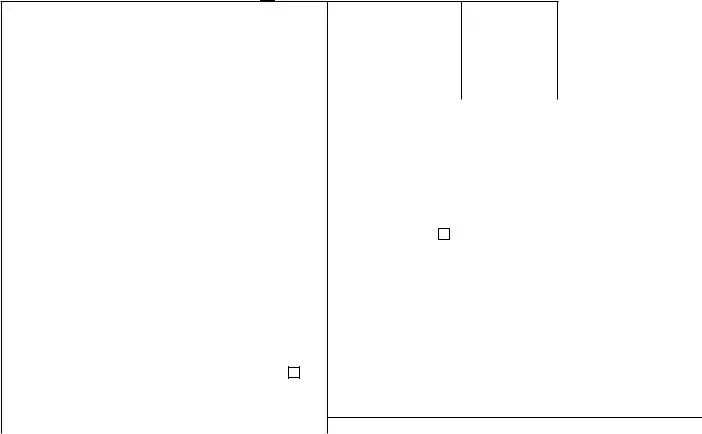

IRS 1099-MISC Example

Attention:

Copy A of this form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. The official printed version of Copy A of this IRS form is scannable, but the online version of it, printed from this website, is not. Do not print and file copy A downloaded from this website; a penalty may be imposed for filing with the IRS information return forms that can’t be scanned. See part O in the current General Instructions for Certain Information Returns, available at IRS.gov/Form1099, for more information about penalties.

Please note that Copy B and other copies of this form, which appear in black, may be downloaded and printed and used to satisfy the requirement to provide the information to the recipient.

If you have 10 or more information returns to file, you may be required to file

If you have fewer than 10 information returns to file, we strongly encourage you to

See Publications 1141, 1167, and 1179 for more information about printing these forms.

9595 |

|

VOID |

CORRECTED |

|

|

|

|

|

|

|||

PAYER’S name, street address, city or town, state or province, country, ZIP |

1 |

Rents |

OMB No. |

|

|

|||||||

or foreign postal code, and telephone no. |

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

$ |

|

Form |

|

Miscellaneous |

||||

|

|

|

|

2 |

Royalties |

(Rev. January 2024) |

|

Information |

||||

|

|

|

|

|

|

For calendar year |

|

|

||||

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

Other income |

4 |

Federal income tax withheld |

Copy A |

||||

|

|

|

|

$ |

|

$ |

|

|

|

|

For |

|

PAYER’S TIN |

RECIPIENT’S TIN |

|

5 |

Fishing boat proceeds |

6 |

Medical and health care |

Internal Revenue |

|||||

|

|

|

|

|

|

|

payments |

Service Center |

||||

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$ |

|

$ |

|

|

|

|

File with Form 1096. |

|

RECIPIENT’S name |

|

|

7 |

Payer made direct sales |

8 |

Substitute payments in lieu |

For Privacy Act |

|||||

|

|

|

|

|

totaling $5,000 or more of |

|

of dividends or interest |

and Paperwork |

||||

|

|

|

|

|

consumer products to |

$ |

|

|

|

|

||

|

|

|

|

|

recipient for resale |

|

|

|

|

Reduction Act |

||

Street address (including apt. no.) |

|

|

9 |

Crop insurance proceeds |

10 |

Gross proceeds paid to an |

Notice, see the |

|||||

|

|

|

|

|

|

|

attorney |

current General |

||||

|

|

|

|

$ |

|

$ |

|

|

|

|

Instructions for |

|

|

|

|

|

|

|

|

|

|

Certain |

|||

City or town, state or province, country, and ZIP or foreign postal code |

11 |

Fish purchased for resale |

12 |

Section 409A deferrals |

||||||||

Information |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

$ |

|

$ |

|

|

|

|

Returns. |

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

13 FATCA filing |

14 |

Excess golden parachute |

15 |

Nonqualified deferred |

|

||||

|

|

|

requirement |

|

payments |

|

compensation |

|

||||

|

|

|

|

$ |

|

$ |

|

|

|

|

|

|

Account number (see instructions) |

|

|

2nd TIN not. |

16 |

State tax withheld |

17 |

State/Payer’s state no. |

18 State income |

||||

|

|

|

|

$ |

|

|

|

|

|

|

$ |

|

|

|

|

|

$ |

|

|

|

|

|

|

$ |

|

Form |

Cat. No. 14425J |

www.irs.gov/Form1099MISC |

|

Department of the Treasury - Internal Revenue Service |

||||||||

Do Not Cut or Separate Forms on This Page — Do Not Cut or Separate Forms on This Page

|

VOID |

CORRECTED |

|

|

|

|

|

|

|

||

PAYER’S name, street address, city or town, state or province, country, ZIP |

1 |

Rents |

OMB No. |

|

|

|

|||||

or foreign postal code, and telephone no. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$ |

|

Form |

|

Miscellaneous |

||||

|

|

|

2 |

Royalties |

(Rev. January 2024) |

|

|

Information |

|||

|

|

|

|

|

For calendar year |

|

|

|

|||

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

Other income |

4 |

Federal income tax withheld |

|

Copy 1 |

|||

|

|

|

$ |

|

$ |

|

|

|

|

|

For State Tax |

PAYER’S TIN |

RECIPIENT’S TIN |

|

5 |

Fishing boat proceeds |

6 |

Medical and health care |

|

Department |

|||

|

|

|

|

|

|

payments |

|

|

|||

|

|

|

$ |

|

$ |

|

|

|

|

|

|

RECIPIENT’S name |

|

|

7 |

Payer made direct sales |

8 |

Substitute payments in lieu |

|

|

|||

|

|

|

|

totaling $5,000 or more of |

|

of dividends or interest |

|

|

|||

|

|

|

|

consumer products to |

$ |

|

|

|

|

|

|

|

|

|

|

recipient for resale |

|

|

|

|

|

|

|

Street address (including apt. no.) |

|

|

9 |

Crop insurance proceeds |

10 |

Gross proceeds paid to an |

|

|

|||

|

|

|

|

|

|

attorney |

|

|

|||

|

|

|

$ |

|

$ |

|

|

|

|

|

|

City or town, state or province, country, and ZIP or foreign postal code |

11 |

Fish purchased for resale |

12 |

Section 409A deferrals |

|

|

|||||

|

|

|

$ |

|

$ |

|

|

|

|

|

|

|

|

13 FATCA filing |

14 |

Excess golden parachute |

15 |

Nonqualified deferred |

|

|

|||

|

|

requirement |

|

payments |

|

compensation |

|

|

|||

|

|

|

$ |

|

$ |

|

|

|

|

|

|

Account number (see instructions) |

|

|

16 |

State tax withheld |

17 |

State/Payer’s state no. |

|

18 State income |

|||

|

|

|

$ |

|

|

|

|

|

|

|

$ |

|

|

|

$ |

|

|

|

|

|

|

|

$ |

Form |

|

www.irs.gov/Form1099MISC |

|

Department of the Treasury - Internal Revenue Service |

|||||||

CORRECTED (if checked)

CORRECTED (if checked)

PAYER’S name, street address, city or town, state or province, country, ZIP 1 Rents |

OMB No. |

or foreign postal code, and telephone no. |

|

|

|

|

$ |

Form |

Miscellaneous |

|||||

|

|

|

2 Royalties |

(Rev. January 2024) |

|

|

Information |

|||

|

|

|

|

For calendar year |

|

|

||||

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

3 Other income |

4 Federal income tax withheld |

Copy B |

|||||

|

|

|

$ |

$ |

|

|

|

|

|

For Recipient |

PAYER’S TIN |

RECIPIENT’S TIN |

5 Fishing boat proceeds |

6 |

Medical and health care |

|

|

||||

|

|

|

|

|

payments |

|

|

|||

|

|

|

$ |

$ |

|

|

|

|

|

|

RECIPIENT’S name |

|

|

7 Payer made direct sales |

8 |

Substitute payments in lieu |

|

This is important tax |

|||

|

|

|

totaling $5,000 or more of |

|

of dividends or interest |

|

||||

|

|

|

consumer products to |

$ |

|

|

|

|

|

information and is |

|

|

|

recipient for resale |

|

|

|

|

|

being furnished to |

|

Street address (including apt. no.) |

|

|

9 Crop insurance proceeds |

10 |

Gross proceeds paid to an |

|

the IRS. If you are |

|||

|

|

|

|

|

attorney |

|

required to file a |

|||

|

|

|

$ |

$ |

|

|

|

|

|

return, a negligence |

|

|

|

|

|

|

|

|

penalty or other |

||

City or town, state or province, country, and ZIP or foreign postal code |

11 Fish purchased for resale |

12 |

Section 409A deferrals |

|

sanction may be |

|||||

|

|

|

|

|

|

|

|

|

|

imposed on you if |

|

|

|

$ |

$ |

|

|

|

|

|

this income is |

|

|

|

|

|

|

|

|

taxable and the IRS |

||

|

|

13 FATCA filing 14 Excess golden parachute |

15 |

Nonqualified deferred |

|

determines that it |

||||

|

|

requirement |

payments |

|

compensation |

|

has not been |

|||

|

|

|

$ |

$ |

|

|

|

|

|

reported. |

|

|

|

|

|

|

|

|

|

||

Account number (see instructions) |

|

|

16 State tax withheld |

17 |

State/Payer’s state no. |

|

18 State income |

|||

|

|

|

$ |

|

|

|

|

|

|

$ |

|

|

|

$ |

|

|

|

|

|

|

$ |

Form |

(keep for your records) |

www.irs.gov/Form1099MISC |

|

Department of the Treasury - Internal Revenue Service |

||||||

Instructions for Recipient

Recipient’s taxpayer identification number (TIN). For your protection, this form may show only the last four digits of your social security number (SSN), individual taxpayer identification number (ITIN), adoption taxpayer identification number (ATIN), or employer identification number (EIN). However, the payer has reported your complete TIN to the IRS.

Account number. May show an account or other unique number the payer assigned to distinguish your account.

Amounts shown may be subject to

Form

Box 1. Report rents from real estate on Schedule E (Form 1040). However, report rents on Schedule C (Form 1040) if you provided significant services to the tenant, sold real estate as a business, or rented personal property as a business. See Pub. 527.

Box 2. Report royalties from oil, gas, or mineral properties; copyrights; and patents on Schedule E (Form 1040). However, report payments for a working interest as explained in the Schedule E (Form 1040) instructions. For royalties on timber, coal, and iron ore, see Pub. 544.

Box 3. Generally, report this amount on the “Other income” line of Schedule 1 (Form 1040) and identify the payment. The amount shown may be payments received as the beneficiary of a deceased employee, prizes, awards, taxable damages, Indian gaming profits, or other taxable income. See Pub. 525. If it is trade or business income, report this amount on Schedule C or F (Form 1040).

Box 4. Shows backup withholding or withholding on Indian gaming profits. Generally, a payer must backup withhold if you did not furnish your TIN. See Form

Box 5. Shows the amount paid to you as a fishing boat crew member by the operator, who considers you to be

Box 6. For individuals, report on Schedule C (Form 1040).

Box 7. If checked, consumer products totaling $5,000 or more were sold to you for resale, on a

Box 8. Shows substitute payments in lieu of dividends or

Box 9. Report this amount on Schedule F (Form 1040).

Box 10. Shows gross proceeds paid to an attorney in connection with legal services. Report only the taxable part as income on your return.

Box 11. Shows the amount of cash you received for the sale of fish if you are in the trade or business of catching fish.

Box 12. May show current year deferrals as a nonemployee under a nonqualified deferred compensation (NQDC) plan that is subject to the requirements of section 409A plus any earnings on current and prior year deferrals.

Box 13. If the FATCA filing requirement box is checked, the payer is reporting on this Form 1099 to satisfy its account reporting requirement under chapter 4 of the Internal Revenue Code. You may also have a filing requirement. See the Instructions for Form 8938.

Box 14. Shows your total compensation of excess golden parachute payments subject to a 20% excise tax. See your tax return instructions for where to report.

Box 15. Shows income as a nonemployee under an NQDC plan that does not meet the requirements of section 409A. Any amount included in box 12 that is currently taxable is also included in this box. Report this amount as income on your tax return. This income is also subject to a substantial additional tax to be reported on Form 1040,

Boxes

Future developments. For the latest information about developments related to Form

Free File Program. Go to www.irs.gov/FreeFile to see if you qualify for

CORRECTED (if checked)

CORRECTED (if checked)

PAYER’S name, street address, city or town, state or province, country, ZIP 1 Rents |

OMB No. |

or foreign postal code, and telephone no. |

|

|

|

|

$ |

|

Form |

Miscellaneous |

|||||

|

|

|

2 Royalties |

|

(Rev. January 2024) |

|

|

Information |

|||

|

|

|

|

|

For calendar year |

|

|

||||

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

3 Other income |

4 |

Federal income tax withheld |

|

Copy 2 |

||||

|

|

|

$ |

$ |

|

|

|

|

|

To be filed with |

|

PAYER’S TIN |

RECIPIENT’S TIN |

5 Fishing boat proceeds |

6 |

Medical and health care |

|

recipient’s state |

|||||

|

|

|

|

|

|

payments |

|

income tax return, |

|||

|

|

|

|

|

|

|

|

|

|

|

when required. |

|

|

|

$ |

$ |

|

|

|

|

|

|

|

RECIPIENT’S name |

|

|

7 Payer made direct sales |

8 |

Substitute payments in lieu |

|

|

||||

|

|

|

totaling $5,000 or more of |

|

|

of dividends or interest |

|

|

|||

|

|

|

consumer products to |

$ |

|

|

|

|

|

|

|

|

|

|

recipient for resale |

|

|

|

|

|

|

||

Street address (including apt. no.) |

|

|

9 Crop insurance proceeds |

10 |

Gross proceeds paid to an |

|

|

||||

|

|

|

|

|

|

attorney |

|

|

|||

|

|

|

$ |

$ |

|

|

|

|

|

|

|

City or town, state or province, country, and ZIP or foreign postal code |

11 Fish purchased for resale |

12 |

Section 409A deferrals |

|

|

||||||

|

|

|

$ |

$ |

|

|

|

|

|

|

|

|

|

13 FATCA filing 14 Excess golden parachute |

15 |

Nonqualified deferred |

|

|

|||||

|

|

requirement |

payments |

|

|

compensation |

|

|

|||

|

|

|

$ |

$ |

|

|

|

|

|

|

|

Account number (see instructions) |

|

|

16 State tax withheld |

17 |

State/Payer’s state no. |

|

18 State income |

||||

|

|

|

$ |

|

|

|

|

|

|

|

$ |

|

|

|

$ |

|

|

|

|

|

|

|

$ |

Form |

www.irs.gov/Form1099MISC |

|

|

Department of the Treasury - Internal Revenue Service |

|||||||