Fill Out a Valid 14653 Template

Guide to Writing 14653

Filling out Form 14653 is an important step for U.S. persons residing outside the United States who are seeking to resolve their tax obligations under the Streamlined Foreign Offshore Procedures. After completing this form, you will need to submit it along with any required documentation to the IRS. Ensure that all information is accurate and complete to avoid delays in processing your submission.

- Obtain the Form: Download Form 14653 from the IRS website or request a physical copy.

- Fill in Your Personal Information: Provide your name(s), Tax Identification Number(s), telephone number, mailing address, city, state, and ZIP code at the top of the form.

- Indicate Certification: Confirm that you are submitting delinquent or amended income tax returns for the last three years. List the years, the amount of tax owed, and any interest due.

- Detail Your Residency Status: Complete the section regarding your residency status. Indicate whether you were physically outside the U.S. for at least 330 full days for each of the relevant years.

- Provide a Statement of Facts: Write a narrative explaining your failure to report all income, pay all tax, and submit required information returns, including FBARs. Include specific reasons, your personal and financial background, and details about your foreign financial accounts.

- Sign the Form: Under penalties of perjury, sign and date the form. If filing jointly, ensure both taxpayers sign.

- Prepare Additional Documentation: If applicable, attach any computations or additional information required for your residency status.

- Submit the Form: Send the completed form and any attachments to the appropriate IRS address as indicated in the instructions.

Document Breakdown

| Fact Name | Description |

|---|---|

| Purpose of Form | Form 14653 is used by U.S. persons residing outside the United States to certify their eligibility for the Streamlined Foreign Offshore Procedures, allowing them to rectify past tax compliance issues. |

| Eligibility Requirements | To qualify, individuals must have been physically outside the U.S. for at least 330 full days in one or more of the last three years and meet other specified conditions. |

| Non-Willful Conduct | The form requires taxpayers to assert that their failure to report income was due to non-willful conduct, which encompasses negligence or misunderstandings regarding tax obligations. |

| Record Retention | Taxpayers must retain records related to their income and foreign financial assets for three years from the date of certification and FBAR records for six years. |

| Joint Certification | If spouses are filing jointly, both must meet the non-residency requirements, and they need to provide individual statements if their reasons for non-compliance differ. |

FAQ

-

What is Form 14653?

Form 14653 is a certification form used by U.S. persons residing outside the United States. It is part of the Streamlined Foreign Offshore Procedures, which help individuals who failed to report income and pay taxes on foreign financial assets. By submitting this form, taxpayers can rectify their past mistakes and avoid penalties.

-

Who needs to fill out Form 14653?

This form is for U.S. citizens and lawful permanent residents living abroad who have not reported income from foreign financial assets. If you meet the eligibility requirements for the Streamlined Foreign Offshore Procedures, you should complete this form.

-

What information do I need to provide on Form 14653?

You will need to provide your name, taxpayer identification number (TIN), contact information, and details about your residency status. Additionally, you must list the years for which you are submitting delinquent or amended tax returns and the amounts of tax and interest owed for each year.

-

What are the eligibility requirements for the Streamlined Foreign Offshore Procedures?

To be eligible, you must have failed to report income due to non-willful conduct, such as negligence or misunderstanding of the law. You must also have been physically outside the U.S. for at least 330 full days in one or more of the last three years and not have had a U.S. abode during that time.

-

What happens if I submit incorrect information on Form 14653?

If you provide incorrect information, it may lead to a balance due notice or a refund. More seriously, if the IRS finds evidence of willfulness or fraud, it could trigger an examination or investigation, resulting in penalties or criminal charges.

-

Do I need to keep records after submitting Form 14653?

Yes, you must retain all records related to your income and assets for three years from the date of certification. If you filed delinquent FBARs, keep records related to those accounts for six years.

-

What is the significance of the statement of facts?

The statement of facts is crucial. It must explain your reasons for failing to report income and pay taxes. Be honest and thorough, including all relevant details about your financial background and any professional advice you received.

-

Can both spouses file a joint certification?

Yes, both spouses can file a joint certification. However, both must meet the non-residency requirements. If they have different reasons for their failures, each spouse must provide their individual reasons in the statement of facts.

-

What if I want to seek a refund after filing Form 14653?

If you seek a refund for taxes or interest paid on omitted income, you may lose the favorable terms of the Streamlined Procedures. Be cautious, as this could complicate your situation.

-

How long does it take to complete Form 14653?

The estimated average time to complete the form is about eight hours. This can vary based on your individual circumstances, so plan accordingly.

Fill out Other Forms

Dd 214 - The DD Form 214 corroborates the eligibility of veterans for various military-related services.

U.S. Corporation Income Tax Return - Understanding the requirements of Form 1120 can help prevent common filing mistakes.

The Payroll Check form is not only essential for documenting the wages paid to employees, but it can also be simplified by utilizing a Fillable Blank Check, which ensures that your payroll process is efficient and compliant with necessary regulations.

Code of Armor - A captivating design full of historical significance.

14653 Example

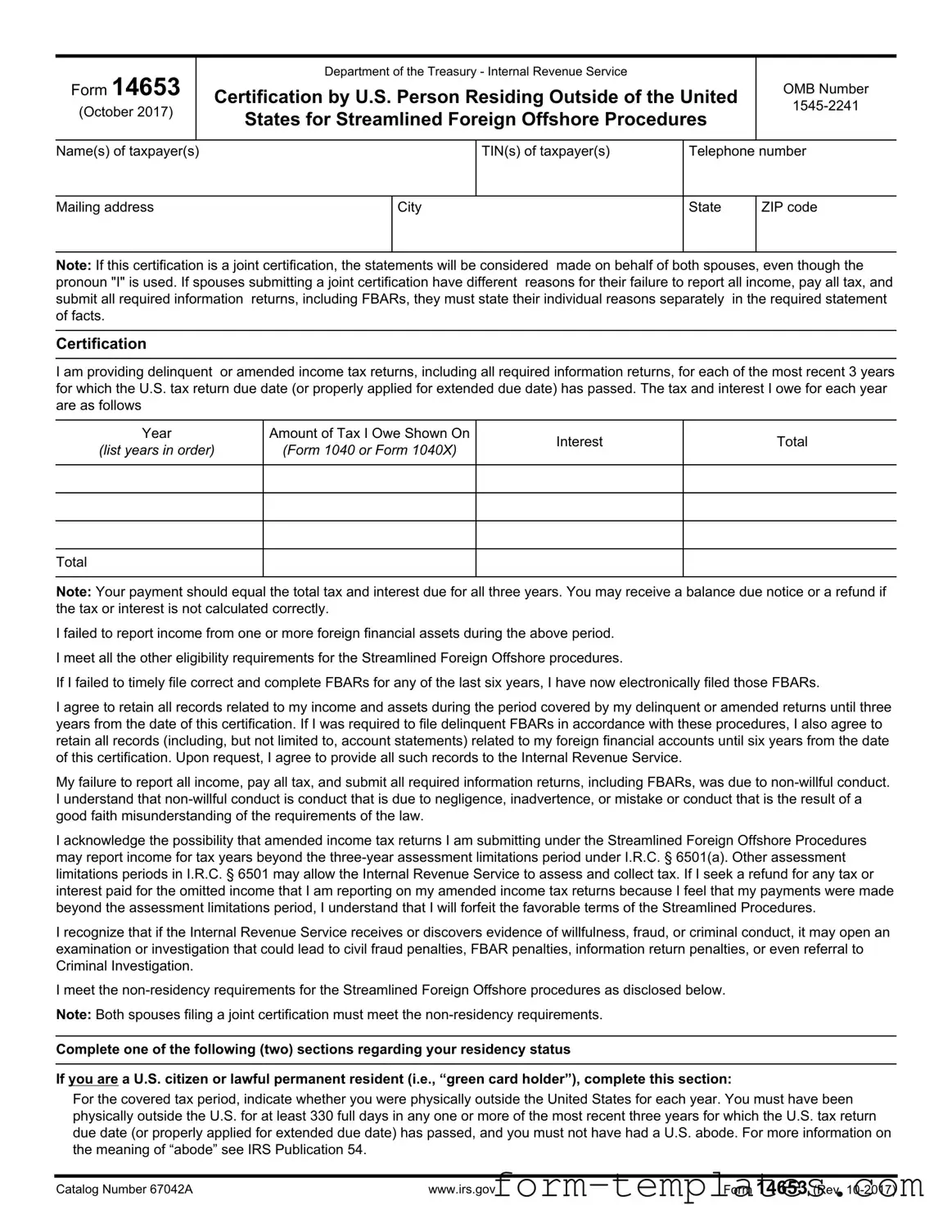

Form 14653

(October 2017)

Department of the Treasury - Internal Revenue Service

Certification by U.S. Person Residing Outside of the United

States for Streamlined Foreign Offshore Procedures

OMB Number

Name(s) of taxpayer(s)

TIN(s) of taxpayer(s)

Telephone number

Mailing address

City

State

ZIP code

Note: If this certification is a joint certification, the statements will be considered made on behalf of both spouses, even though the pronoun "I" is used. If spouses submitting a joint certification have different reasons for their failure to report all income, pay all tax, and submit all required information returns, including FBARs, they must state their individual reasons separately in the required statement of facts.

Certification

I am providing delinquent or amended income tax returns, including all required information returns, for each of the most recent 3 years for which the U.S. tax return due date (or properly applied for extended due date) has passed. The tax and interest I owe for each year are as follows

Year

(list years in order)

Amount of Tax I Owe Shown On

(Form 1040 or Form 1040X)

Interest

Total

Total

Note: Your payment should equal the total tax and interest due for all three years. You may receive a balance due notice or a refund if the tax or interest is not calculated correctly.

I failed to report income from one or more foreign financial assets during the above period.

I meet all the other eligibility requirements for the Streamlined Foreign Offshore procedures.

If I failed to timely file correct and complete FBARs for any of the last six years, I have now electronically filed those FBARs.

I agree to retain all records related to my income and assets during the period covered by my delinquent or amended returns until three years from the date of this certification. If I was required to file delinquent FBARs in accordance with these procedures, I also agree to retain all records (including, but not limited to, account statements) related to my foreign financial accounts until six years from the date of this certification. Upon request, I agree to provide all such records to the Internal Revenue Service.

My failure to report all income, pay all tax, and submit all required information returns, including FBARs, was due to

I acknowledge the possibility that amended income tax returns I am submitting under the Streamlined Foreign Offshore Procedures may report income for tax years beyond the

I recognize that if the Internal Revenue Service receives or discovers evidence of willfulness, fraud, or criminal conduct, it may open an examination or investigation that could lead to civil fraud penalties, FBAR penalties, information return penalties, or even referral to Criminal Investigation.

I meet the

Note: Both spouses filing a joint certification must meet the

Complete one of the following (two) sections regarding your residency status

If you are a U.S. citizen or lawful permanent resident (i.e., “green card holder”), complete this section:

For the covered tax period, indicate whether you were physically outside the United States for each year. You must have been physically outside the U.S. for at least 330 full days in any one or more of the most recent three years for which the U.S. tax return due date (or properly applied for extended due date) has passed, and you must not have had a U.S. abode. For more information on the meaning of “abode” see IRS Publication 54.

Catalog Number 67042A |

www.irs.gov |

Form 14653 (Rev. |

Page of

I was physically outside the United States for at least 330 full days (answer Yes or No for each year)

Year

Yes

No

Both spouses filing a joint certification must meet the

If you are not a U.S. citizen or lawful permanent resident, complete this section:

If you are not a U.S. citizen or a lawful permanent resident, please attach to this certification your computation showing that you did not meet the substantial presence test under I.R.C. sec. 7701(b)(3). Your computation must disclose the number of days you were present in the U.S. for the three years included in your Streamlined Foreign Offshore Procedures submission and the previous two years. If you do not attach a complete computation showing that you did not meet the substantial presence test, your submission will be considered incomplete and your submission will not qualify for the Streamlined Foreign Offshore Procedures.

Both spouses filing a joint certification must meet the

Note: You must provide specific facts on this form or on a signed attachment explaining your failure to report all income, pay all tax, and submit all required information returns, including FBARs. Any submission that does not contain a narrative statement of facts will be considered incomplete and will not qualify for the streamlined penalty relief.

Provide specific reasons for your failure to report all income, pay all tax, and submit all required information returns, including FBARs. Include the whole story including favorable and unfavorable facts. Specific reasons, whether favorable or unfavorable to you, should include your personal background, financial background, and anything else you believe is relevant to your failure to report all income, pay all tax, and submit all required information returns, including FBARs. Additionally, explain the source of funds in all of your foreign financial accounts/assets. For example, explain whether you inherited the account/asset, whether you opened it while residing in a foreign country, or whether you had a business reason to open or use it. And explain your contacts with the account/asset including withdrawals, deposits, and investment/ management decisions. Provide a complete story about your foreign financial account/asset. If you relied on a professional advisor, provide the name, address, and telephone number of the advisor and a summary of the advice. If married taxpayers submitting a joint certification have different reasons, provide the individual reasons for each spouse separately in the statement of facts. The field below will automatically expand to accommodate your statement of facts.

Catalog Number 67042A |

www.irs.gov |

Form 14653 (Rev. |

Page of

Under penalties of perjury, I declare that I have examined this certification and all accompanying schedules and statements, and to the best of my knowledge and belief, they are true, correct, and complete.

Signature of Taxpayer |

Name of Taxpayer |

Date |

|

|

|

Signature of Taxpayer (if joint certification) |

Name of Taxpayer (if joint certification) |

Date |

|

|

|

For Estates Only

Signature of Fiduciary |

Date |

|

|

Title of Fiduciary (e.g., executor or administrator)

Name of Fiduciary

For Paid Preparer Use Only (the signature of taxpayer(s) or fiduciary is required even if this form is signed by a paid preparer)

Signature of Preparer |

Name of Preparer |

|

|

Date |

|

|

|

|

|

Firm’s name |

|

|

|

Firm’s EIN |

|

|

|

|

|

Firm’s address |

City |

|

State |

ZIP code |

|

|

|

|

|

Telephone number |

PTIN |

|

|

Check if |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Do you want to allow another person to discuss this form with the IRS |

Yes (complete information below) |

No |

||

|

|

|

|

|

Designee’s name |

|

|

Telephone number |

|

|

|

|

|

|

Privacy Act and Paperwork Reduction Notice

We ask for the information on this certification by U.S. person residing in the United States for streamlined domestic offshore procedures to carry out the Internal Revenue laws of the United States. Our authority to ask for information is sections 6001, 6109, 7801, 7803 and the regulations thereunder. This information will be used to determine and collect the correct amount of tax under the terms of the streamlined filing compliance program. You are not required to apply for participation in the streamlined filing compliance program. If you choose to apply, however, you are required to provide all the information requested on the streamlined certification. You are not required to provide the information requested on a document that is subject to the Paperwork Reduction Act unless the document displays a valid OMB control number. Books or records relating to a document or its instructions must be retained as long as their contents may become material in the administration of any Internal Revenue law. Generally, tax returns and return information are confidential, as required by section 6103. Section 6103, however, allows or requires the Internal Revenue Service to disclose or give this information to others as described in the Internal Revenue Code. For example, we may disclose this information to the Department of Justice to enforce the tax laws, both civil and criminal, and to cities, states, the District of Columbia, and U.S. commonwealths or possessions to carry out their tax laws. We may also disclose this information to other countries under a tax treaty, to federal and state agencies to enforce federal nontax criminal laws, or to federal law enforcement and intelligence agencies to combat terrorism. Failure to provide this information may delay or prevent processing your application. Providing false information may subject you to penalties. The time needed to complete and submit the streamlined certification will vary depending on individual circumstances. The estimated average time is: 8 hours

Catalog Number 67042A |

www.irs.gov |

Form 14653 (Rev. |